The financial landscape is preparing to shift as baby boomers pass on an estimated $85 trillion to younger generations. The institutions positioned to benefit most from this “Great Wealth Transfer,” will be the institutions capable of delivering the seamless, intuitive and personalized experiences younger consumers now expect.

Gen Z and millennials are not comparing their financial institution solely against other banks. They are comparing every interaction against the best digital experiences they use daily — from e-commerce and streaming platforms to payment apps and social platforms.

For community and regional financial institutions, this creates both urgency and opportunity. Institutions that combine trusted financial relationships with modern digital experiences can compete more effectively for the next generation of primary banking relationships.

Younger consumers are seeking financial institutions that can meet their digital banking expectations while still delivering trusted guidance and support.

Younger consumers are seeking financial institutions that can meet their digital banking expectations while still delivering trusted guidance and support.

Key Takeaways

- Gen Z and millennials increasingly expect banking experiences that are intuitive, personalized, and digitally seamless.

- Younger consumers are more willing to switch financial institutions when digital experiences fall short.

- Digital convenience is now foundational to relationship banking, not separate from it.

- Financial wellness tools, proactive insight, and connected experiences are becoming major differentiators.

- Institutions that modernize engagement while maintaining trusted relationships are better positioned to compete for long-term loyalty, and deposits.

Attracting the Youngest Consumers

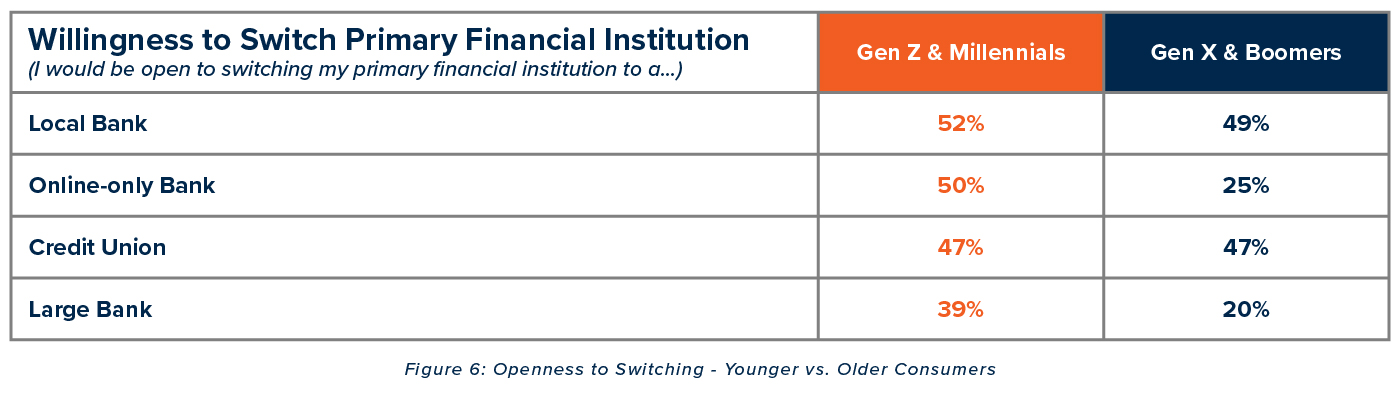

Today, 79% of Gen Z and 69% of millennials have chosen a large bank as their primary financial institution. However, according to a study from The Harris Poll, about half of younger consumers with a primary large bank relationship are open to switching to a small institution, including a community bank (52%), online-only institution (50%), or credit union (47%).

Unlike previous generations, younger consumers often view banking relationships as highly flexible. Digital account opening, mobile payment ecosystems and embedded financial experiences have reduced switching friction significantly.

As a result, loyalty is increasingly shaped by convenience, relevance, and experience quality rather than institution size or long-standing relationships alone.

These changing expectations are also reshaping how institutions compete for long-term customer relationships and deposits. Financial institutions that fail to modernize engagement risk losing younger consumers earlier in their financial journey.

Explore more in our white paper, Winning the Battle for Deposits.

Gen Z and millennials prefer the convenience of online and mobile banking and are visiting physical branches less often. In fact, when asked about their preferred banking methods, only 10% of Gen Z and millennial respondents said they prefer in-person banking.

For younger consumers, digital convenience is now non-negotiable. With 84% saying the ability to complete banking activities and access finances digitally is essential, financial institutions must develop digital strategies that align with evolving consumer expectations.

But delivering a strong digital experience is no longer just about offering online and mobile banking access. Younger consumers increasingly expect banking experiences that feel intuitive, connected, and personalized across every interaction.

Digital Experiences Now Power Relationship Banking

While Gen Z and millennials prioritize digital convenience, they still value trusted financial guidance — particularly during important financial moments like buying a home, building credit, managing debt, or planning for long-term financial goals.

Increasingly, digital experiences serve as the gateway to relationship banking rather than a replacement for it. Younger consumers expect to move seamlessly between self-service digital interactions and human support when needed.

This creates a meaningful opportunity for community and regional financial institutions. Institutions that combine personalized service with modern digital engagement can differentiate themselves from larger competitors that may struggle to deliver both at scale.

Relationship banking remains important, but the expectations surrounding it are changing. Consumers increasingly want financial institutions that can provide responsive support, proactive communication, and personalized experiences across channels.

What Banking Features Do Young Consumers Want?

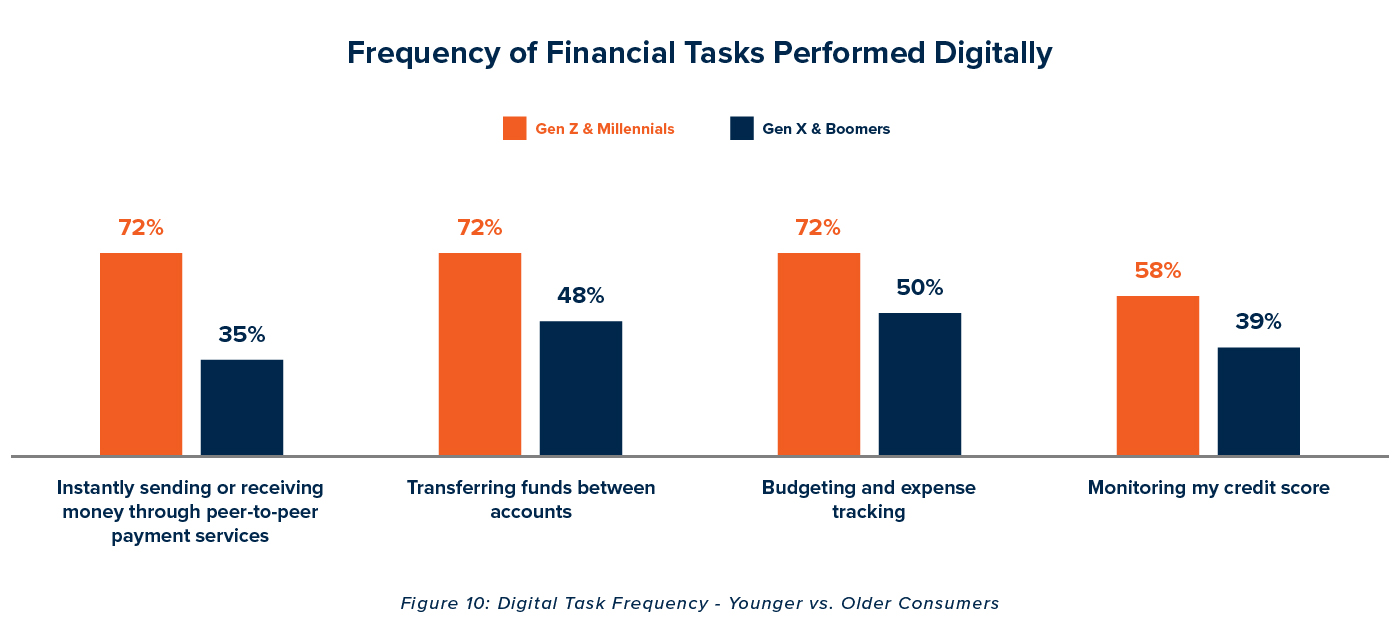

To build loyalty with Gen Z and millennials, financial institutions must deliver modern digital banking experiences centered around the features younger consumers use most. Nearly three quarters frequently use peer-to-peer payments, transfer funds between accounts, and rely on budgeting and expense tracking tools, while more than half regularly monitor their credit score.

But younger consumers increasingly expect more than transactional functionality. They want proactive experiences that help them better manage their finances through personalized insights, predictive alerts, and financial wellness tools.

Rather than simply displaying account information, leading digital banking experiences help consumers understand and improve their financial position. For many Gen Z and millennial consumers, the ideal banking experience feels less reactive and more advisory.

Build Connected Digital Banking Experiences

Younger consumers expect banking experiences to integrate naturally into the digital ecosystems they already use every day. Embedded payment experiences, real-time notifications, and seamless cross-device functionality are increasingly shaping expectations.

Digital wallet integration remains especially important, with younger consumers showing significantly stronger preference for mobile-first payment experiences than older generations.

At the same time, consumers increasingly expect fast, secure and frictionless movement between channels and devices. Whether engaging through a mobile app, digital wallet, online banking platform, or in-person interaction, consistency and ease of use are critical.

To stay competitive, financial institutions should focus on building connected digital experiences that reduce friction and create continuity across the customer journey.

Balance Convenience with Security and Trust

As fraud, scams and identity theft continue to rise, trust has become an increasingly important part of the digital banking experience.

Gen Z and millennial consumers want transparency around how their information is protected, as well as tools that help them monitor account activity, manage alerts, and respond quickly to suspicious behavior.

Financial institutions that can combine convenience with strong security experiences are better positioned to build long-term trust and loyalty with younger generations.

Embrace the Opportunity to Innovate

Successful preparation for the Great Wealth Transfer will depend on more than adding digital features. The institutions that win the next generation of primary banking relationships will be those that combine modern digital engagement with trusted financial relationships, personalized guidance, and seamless service across channels.

While Gen Z consumers often prioritize speed, convenience, and mobile-first experiences, millennials are increasingly focused on financial institutions that can support larger financial milestones and long-term financial goals. Across both generations, expectations around personalization, responsiveness, and ease of use continue to rise.

These shifting preferences also reshaping competition for deposits and long-term customer loyalty. Younger consumers are more willing to move their primary banking relationships when experiences fail to meet expectations, creating both risk and opportunity for financial institutions.

To explore how financial institutions can strengthen loyalty, deepen relationships, and compete more effectively for deposits across generations, read Winning the Battle for Deposits.

Read the white paper

Jennifer Dimenna, Vice President of Product Management

Jennifer Dimenna is Vice President of Product Management at CSI, where she leads teams of product managers, business analysts and user experience designers in developing innovative digital banking solutions. With more than 20 years of experience in product leadership, she combines strategic vision with deep industry expertise. Jennifer began her career after earning a degree in Technical Communication from Georgia Tech and currently resides in Atlanta.